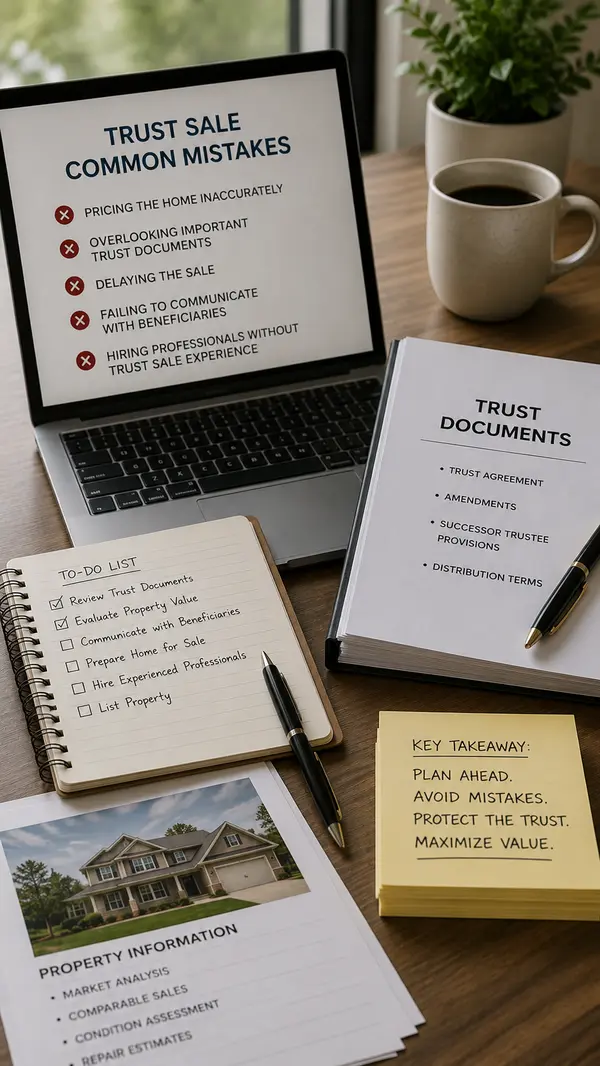

The 10 Biggest Mistakes Trustees Make When Selling Real Estate

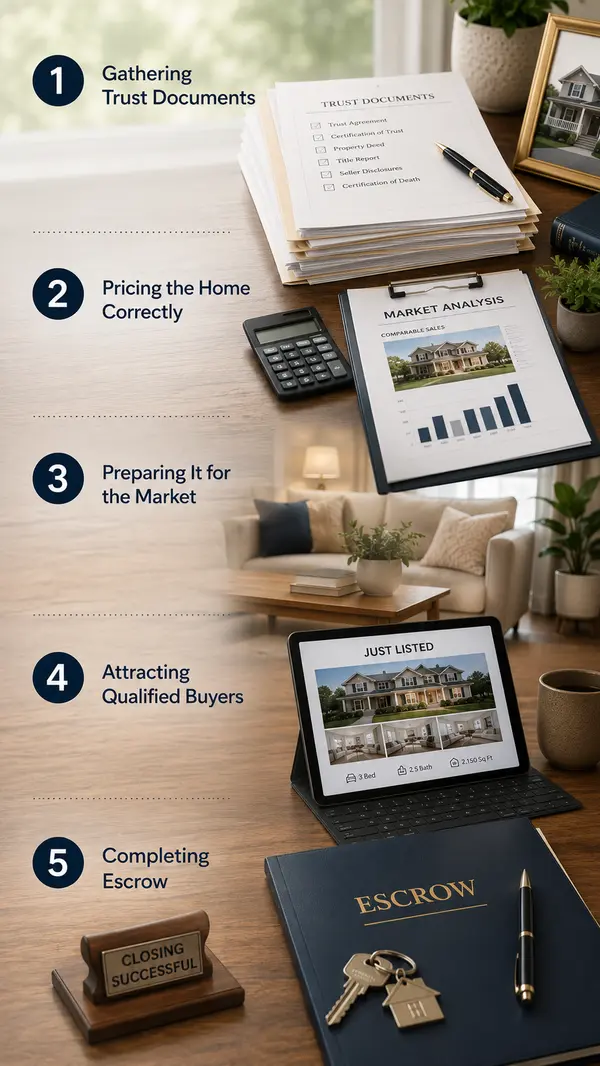

Serving as a trustee is both an honor and a significant legal responsibility. In many cases, trustees are tasked with selling a home that has been in the family for decades while balancing legal obligations, financial considerations, and the emotions of beneficiaries. Unlike a traditional home sal

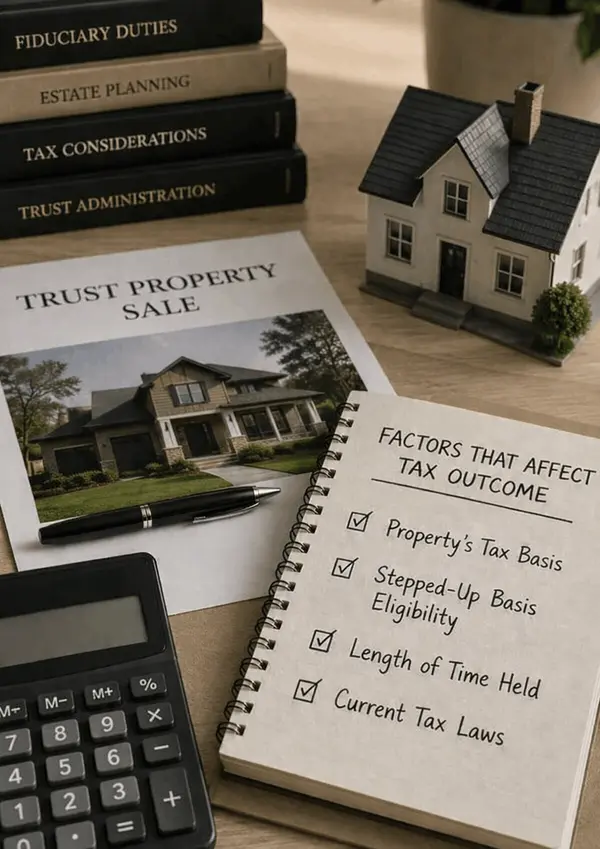

Read MoreCapital Gains and Trust Property Sales: What Trustees Should Know

One of the most common concerns trustees have when preparing to sell a trust-owned home is whether the sale will trigger capital gains taxes. While many trustees understand that taxes may apply, the rules surrounding trusts, inherited property, and the stepped-up basis can be confusing. The good n

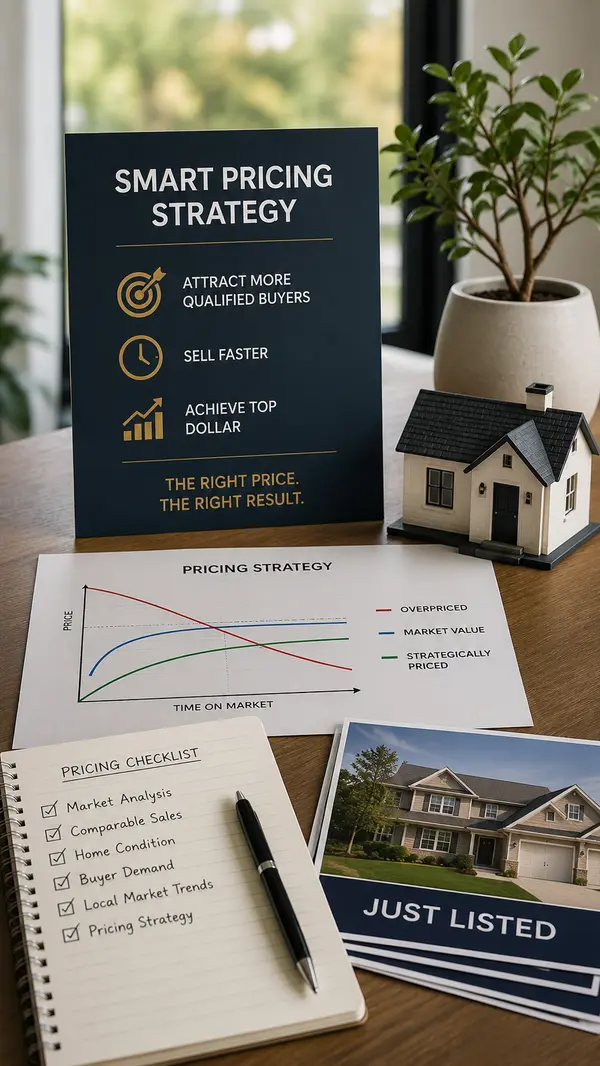

Read MoreHow to Determine the True Value of a Trust Property

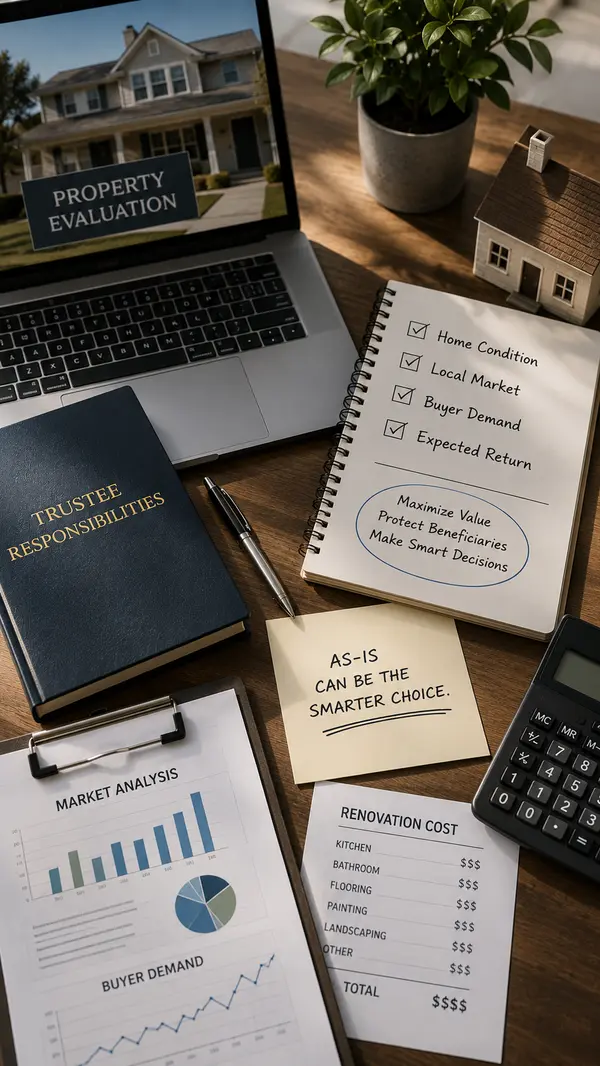

Determining the value of a trust property is one of the most important responsibilities a trustee faces. The listing price you choose can influence everything from how quickly the home sells to how much the beneficiaries ultimately receive. Price it too high, and the property may linger on the mar

Read More

Categories

Recent Posts