How Much Cash Do You Really Need to Buy a Home in Berkeley?

One of the most common questions among buyers relocating to the East Bay, first-time homebuyers, and even high-income professionals is: How much money do I actually need to buy a home in Berkeley?

Many buyers assume they need a 20% down payment and hundreds of thousands of dollars in cash to enter the Berkeley market. While Berkeley is undoubtedly one of the Bay Area's more expensive housing markets, the amount of cash needed varies significantly based on your financing, purchase price, and overall financial strategy.

Understanding the true costs of buying a home can help you prepare, avoid surprises, and determine whether now is the right time to enter the market.

The First Question: What Price Range Are You Shopping In?

Before calculating your cash requirements, you need a realistic understanding of Berkeley home prices.

The amount needed to purchase a home in:

- North Berkeley

- Elmwood

- Claremont

- Thousand Oaks

- Berkeley Hills

- South Berkeley

- West Berkeley

can vary dramatically based on location, condition, and property type.

For example, a condominium, townhouse, and single-family home often require very different financial commitments.

Your target purchase price is the foundation of every affordability calculation.

Do You Really Need 20% Down?

The short answer is no.

While a 20% down payment remains common, many buyers successfully purchase homes with less.

Common Down Payment Options

3%–5% Down

- Available through certain conventional loan programs

- Often used by first-time buyers

- Lower upfront cash requirement

- May require private mortgage insurance (PMI)

10% Down

- Popular among many Bay Area buyers

- Balances affordability and financing flexibility

- May still require mortgage insurance depending on the loan structure

20% Down

- Avoids PMI in many cases

- Often results in stronger financing terms

- Can make offers more competitive in multiple-offer situations

More Than 20% Down

- Common among move-up buyers and relocation clients

- Reduces monthly payments

- May strengthen negotiating position

The right down payment depends on your financial goals, available cash reserves, and long-term plans.

Beyond the Down Payment: Other Costs Buyers Need to Budget For

One of the biggest surprises for first-time buyers is that the down payment is only part of the cash needed to close.

Closing Costs

Most buyers should plan for additional closing costs, which can include:

- Loan origination fees

- Appraisal fees

- Title and escrow charges

- Recording fees

- Homeowner's insurance

- Prepaid property taxes

- Interest adjustments

A good rule of thumb is to budget approximately 2%–4% of the purchase price for closing-related expenses.

Earnest Money Deposit

In Berkeley's competitive market, buyers often submit an earnest money deposit when their offer is accepted.

This deposit is typically credited toward the purchase but requires accessible funds during the transaction.

Moving Expenses

Don't forget the costs associated with:

- Movers

- Storage

- Utility transfers

- Furniture purchases

- Minor repairs or improvements

These expenses can add up quickly after closing.

What About Monthly Costs?

Affordability isn't just about how much cash you need today.

It's also about comfortably managing monthly ownership expenses.

Mortgage Payment

Your monthly mortgage payment depends on:

- Purchase price

- Down payment

- Interest rate

- Loan term

Property Taxes

California property taxes are generally based on the purchase price and can represent a substantial monthly expense.

Homeowners Insurance

Insurance costs vary based on the property's location, age, and coverage needs.

Maintenance and Repairs

Homeownership comes with ongoing maintenance responsibilities. Buyers should budget for future repairs, upgrades, and routine upkeep.

HOA Fees (If Applicable)

Condominiums and some planned communities may include monthly homeowners association dues.

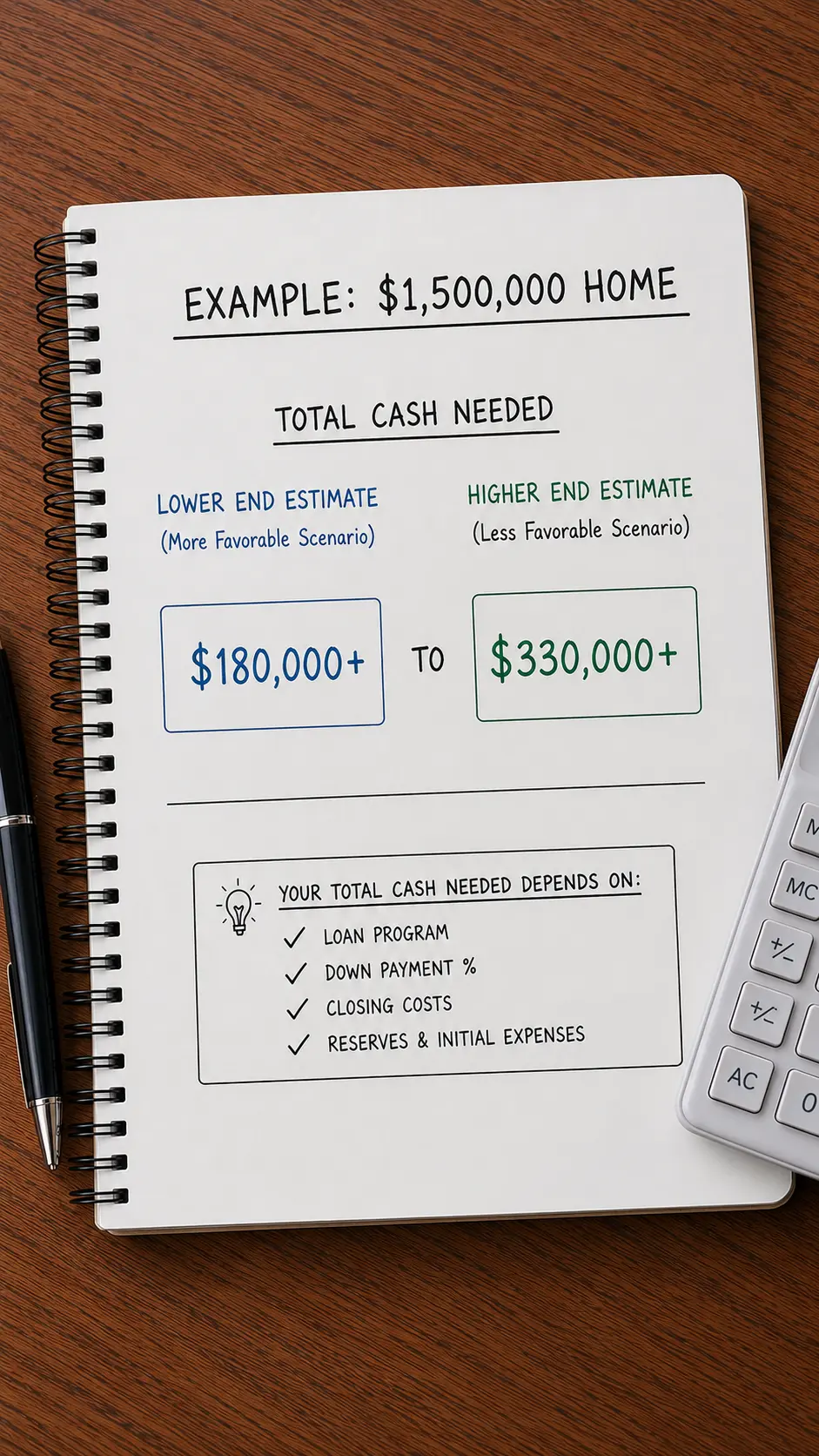

How Much Cash Might a Typical Berkeley Buyer Need?

Let's look at a simplified example.

If a buyer purchases a home for $1.5 million:

Scenario A: 20% Down

- Down payment: $300,000

- Estimated closing costs: $30,000–$60,000

- Recommended reserve funds: Additional savings for emergencies

Total cash needed could exceed $330,000.

Scenario B: 10% Down

- Down payment: $150,000

- Estimated closing costs: $30,000–$60,000

- Reserve funds recommended

Total cash needed may be closer to $180,000–$210,000.

These examples illustrate why working with a lender and real estate professional early in the process is essential.

Why Pre-Approval Matters

Many buyers begin their home search before understanding their actual purchasing power.

A mortgage pre-approval helps determine:

- Maximum purchase price

- Estimated monthly payment

- Available loan programs

- Required cash to close

Pre-approval also strengthens your position when competing against other buyers.

Berkeley Buyers Face Unique Market Conditions

Berkeley remains one of the most competitive housing markets in the East Bay.

Many homes receive multiple offers, particularly in neighborhoods such as:

- North Berkeley

- Elmwood

- Claremont

- Thousand Oaks

- Berkeley Hills

Because of this competition, buyers benefit from understanding not only how much they can afford but also how much flexibility they have when submitting offers.

A well-prepared buyer is often more successful than a buyer scrambling to determine financing after finding the right property.

The Hidden Cost of Waiting

Many buyers focus exclusively on today's prices and interest rates.

However, waiting also has potential costs:

- Future home price appreciation

- Increased competition

- Reduced inventory

- Rising rents

- Lost equity-building opportunities

The decision to buy should be based on personal financial readiness rather than attempting to perfectly time the market.

Work With a Berkeley Real Estate Expert

With seventeen years of experience in residential and investment real estate, Parisa Samimi is recognized as a leading top producer throughout the San Francisco Bay Area. Her background as a real estate appraiser provides buyers with a unique advantage when evaluating property values and determining whether a home represents a sound investment.

Known for her market expertise, attention to detail, and client-first approach, Parisa helps buyers navigate Berkeley's competitive housing market with confidence. From understanding affordability and financing options to evaluating neighborhoods and negotiating offers, she provides strategic guidance every step of the way.

Ready to Find Out What You Can Afford in Berkeley?

Every buyer's financial situation is different.

The amount of cash you need depends on your goals, financing strategy, target neighborhood, and desired property type.

Contact Parisa Samimi today for personalized guidance on buying a home in Berkeley. Whether you're a first-time buyer, relocating to the Bay Area, or planning your next investment, she can help you understand your options and develop a strategy that fits your budget and goals.

Categories

Recent Posts

GET MORE INFORMATION

Parisa Samimi

Founder & Real Estate Broker | License ID: 01858122

Founder & Real Estate Broker License ID: 01858122